As the global tax landscape evolves rapidly, the UAE has embraced the OECD’s Pillar Two framework, reshaping how multinational enterprises (MNEs) and free-zone entities approach corporate tax compliance. With the UAE Ministry of Finance (MoF) issuing critical guidance on the Domestic Minimum Top-Up Tax (DMTT), businesses face new complexities and opportunities to optimize their tax structures under the Global Minimum Tax rules. This article explores the latest Pillar Two developments in the UAE, the implications for free-zone entities, practical approaches to modelling tax exposures, and effective structuring strategies for 2025.

Understanding Pillar Two and the UAE’s Domestic Minimum Top-Up Tax

Pillar Two is part of the OECD’s Inclusive Framework on Base Erosion and Profit Shifting (BEPS), establishing a global minimum effective tax rate (ETR) of 15% for large MNE groups. The UAE’s response is embodied in Cabinet Decision No. 142 of 2024 and subsequent regulations, which introduce the Domestic Minimum Top-Up Tax (DMTT). The DMTT applies when the ETR of a UAE constituent entity falls below the 15% threshold, necessitating a “top-up” payment to align the tax burden with global standards.

Key highlights for UAE entities include:

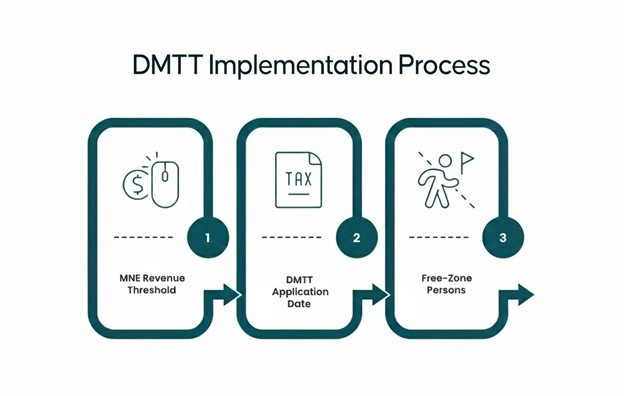

- The Pillar Two regime applies to MNEs with consolidated global revenues exceeding €750 million in at least two of the prior four years.

- The DMTT will be effective from financial years starting on or after January 1, 2025.

- Free-zone persons, including Qualifying Free Zone Persons (QFZPs), are not exempt from the DMTT if they meet the criteria, as clarified in MoF FAQs.

These rules mean many UAE-based groups must reassess their corporate tax exposure carefully, especially regarding entities benefiting from free-zone tax incentives.

Free Zone Clarifications and Their Pillar Two Impact

Recent clarifications by the MoF and the Federal Tax Authority (FTA), particularly Ministerial Decisions No. 229 and 230 of 2025, provide more certainty on the treatment of QFZPs for Pillar Two purposes. These clarifications address aspects such as commodity trading, distribution thresholds, and activities that may disqualify entities from zero-tax treatment under free-zone regimes.

These developments are crucial because:

- Free zone tax exemptions continue to impact the calculation of the ETR denominator, influencing the top-up tax exposure.

- Entities with 0% corporate tax in free zones must ensure genuine economic substance and adhere to specified “safe harbour” criteria. Failure to do so may trigger unexpected Pillar Two top-up tax liabilities.

- The MoF’s approach emphasizes substance over incentives, aligning with international tax principles.

For entities and tax advisors, understanding how free-zone benefits integrate with UAE’s DMTT is essential in tax compliance and advisory work.

Modelling Top-Up Tax Exposure: What Finance Needs to Consider

To navigate Pillar Two successfully, finance teams must conduct robust modelling of potential top-up tax liabilities. The following steps should be part of the Pillar Two UAE tax compliance process:

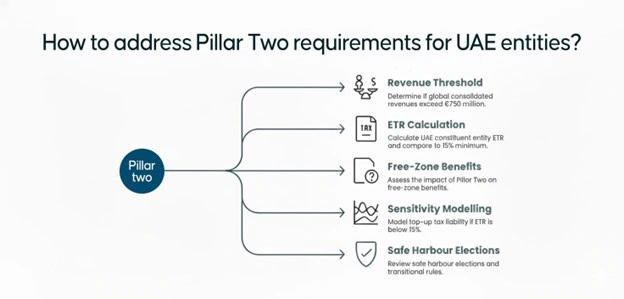

- Confirm if the group’s consolidated global revenues surpass the €750 million threshold in the relevant years.

- Calculate the effective tax rate of UAE constituent entities by analyzing covered taxes and profits within a standardized p&l account format aligned to Pillar Two requirements.

- Evaluate how free-zone tax benefits affect the local ETR and whether these entities remain attractive under the global minimum tax regime.

- Conduct sensitivity testing by modelling different ETR scenarios to identify possible top-up tax liabilities, timing of payments, and overall incremental tax costs.

- Review transitional rules and safe-harbour elections applicable in various jurisdictions, shaping the timing and quantum of tax exposures.

Such thorough Pillar Two modelling enables finance and corporate tax advisory teams to anticipate financial impacts accurately and inform strategic decisions.

Structuring Options: Moving from Compliance to Strategy

Once top-up tax exposures are clearly mapped, businesses may explore a variety of structuring options to optimize their UAE corporate tax position under Pillar Two. Structuring strategies might include:

- Relocating operational functions or profit centres to jurisdictions where the effective tax rate meets or exceeds 15% to avoid DMTT liabilities.

- Reevaluating the substance and economic purpose of free zone entities, especially those involved in trading or holding, to align with Pillar Two’s substance-based criteria.

- Consolidating or rationalizing constituent entities to reduce fragmented calculations of effective tax rates and minimize administrative burdens.

- Considering early elections for transitional filing or safe harbour provisions to manage compliance costs and reduce unexpected tax shocks.

- Embedding Pillar Two modelling into budgeting, financial forecasting, and board-level tax discussions as an integral part of corporate tax strategy.

Proactive structuring not only reduces additional tax charges but also positions businesses competitively in the evolving international tax environment.

Governance and Reporting: Pillar Two as a Board-Level Priority

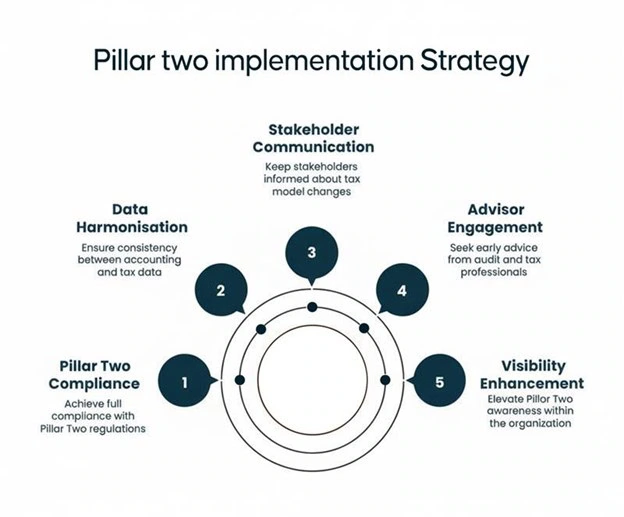

Effective governance and transparent reporting are critical to managing Pillar Two risks and opportunities in the UAE. Tax and finance leaders should:

- Integrate Pillar Two risks into corporate tax risk registers and regularly update board papers to maintain high visibility at executive levels.

- Ensure close alignment between accounting and tax departments since reliable financial data forms the foundation for accurate Pillar Two calculations.

- Engage audit and tax advisors early in the process, as many jurisdictions require comprehensive group-level disclosures and local top-up tax reporting.

- Prepare for stakeholder communications, including banks, licensors, and auditors, clearly outlining the impact of evolving free zone tax treatments on corporate tax models.

Elevating Pillar Two governance helps maintain compliance and facilitates strategic responses to tax reforms.

How ebs Supports UAE Businesses with Pillar Two Readiness

At ebs chartered accountants in Dubai, in-depth UAE local knowledge combined with expertise in international tax reform helps organizations navigate the complexities of Pillar Two and UAE free-zone clarifications. Services include:

- Conducting Pillar Two readiness diagnostics focusing on impact assessment, modelling, and entity screening.

- Modelling top-up tax exposures for UAE constituent entities and multinational tax groups to inform compliance and advisory strategies.

- Reviewing free-zone structuring options in light of the latest MoF and FTA clarifications to align with tax compliance while preserving value.

- Providing governance support with board-ready briefs and expert advice for smooth integration of Pillar Two requirements.

- Driving audit and tax team collaboration to synchronize accounting data and tax calculations.

With a multidisciplinary team spanning tax, transfer pricing, audit, and corporate structuring, ebs empowers UAE businesses to turn global minimum tax compliance into a strategic advantage.

Reach out to us to schedule a Pillar Two readiness workshop and get expert support on restructuring your tax framework for 2025 and beyond.

FAQs

What is Pillar Two and how does it apply in the UAE?

Pillar Two is a global minimum tax framework under the OECD’s Inclusive Framework, setting a minimum effective tax rate (ETR) of 15% for large multinational enterprises (MNEs). In the UAE, the Ministry of Finance introduced the Domestic Minimum Top-Up Tax (DMTT), effective for financial years starting January 1, 2025. It applies to UAE constituent entities of MNEs whose local ETR falls below 15%, requiring a top-up tax payment to meet the minimum threshold.

Are UAE Free Zone entities exempt from Pillar Two top-up tax?

No, free-zone persons, including Qualifying Free Zone Persons (QFZPs), are not automatically exempt from the DMTT. If they meet the €750 million global revenue threshold and their ETR falls below 15%, they are subject to Pillar Two top-up tax. However, entities must ensure sufficient economic substance and meet safe harbour conditions to avoid unintended Pillar Two liabilities.

What thresholds determine if my UAE group is in scope for Pillar Two?

Pillar Two applies to MNE groups with global consolidated revenues exceeding €750 million in at least two of the prior four fiscal years. Groups must also calculate the effective tax rates of their UAE constituent entities compared to the 15% minimum. This assessment triggers whether the top-up tax obligation arises.

What are the key compliance obligations under the UAE DMTT regime?

In-scope MNEs must register for DMTT, file top-up tax returns, and potentially submit Pillar Two information returns alongside regular corporate tax filings. Financial statement disclosures for FY 2025 must include Pillar Two impact assessments aligned with IAS 12 requirements. Early engagement with tax advisors and finance teams is crucial for accurate reporting and governance.

How can UAE businesses structure to minimize Pillar Two top-up tax exposure?

Businesses can consider relocating profit centres to jurisdictions with effective tax rates above 15%, consolidating entities to reduce fragmented calculations, and ensuring that free-zone entities have genuine substance and align with Pillar Two principles. Early adoption of safe harbour elections and integration of Pillar Two modelling into corporate tax strategy help manage risks and compliance costs effectively.