The business landscape in the United Arab Emirates has fundamentally shifted. With the implementation of Federal Decree-Law No. 47 of 2022 introducing comprehensive corporate tax regulations, benchmarking reports have evolved from optional best practices into mandatory compliance tools. For companies conducting transactions with related parties or connected persons, proper benchmarking documentation is no longer a choice; it’s a regulatory necessity.

UAE Transfer Pricing Documentation Requirements

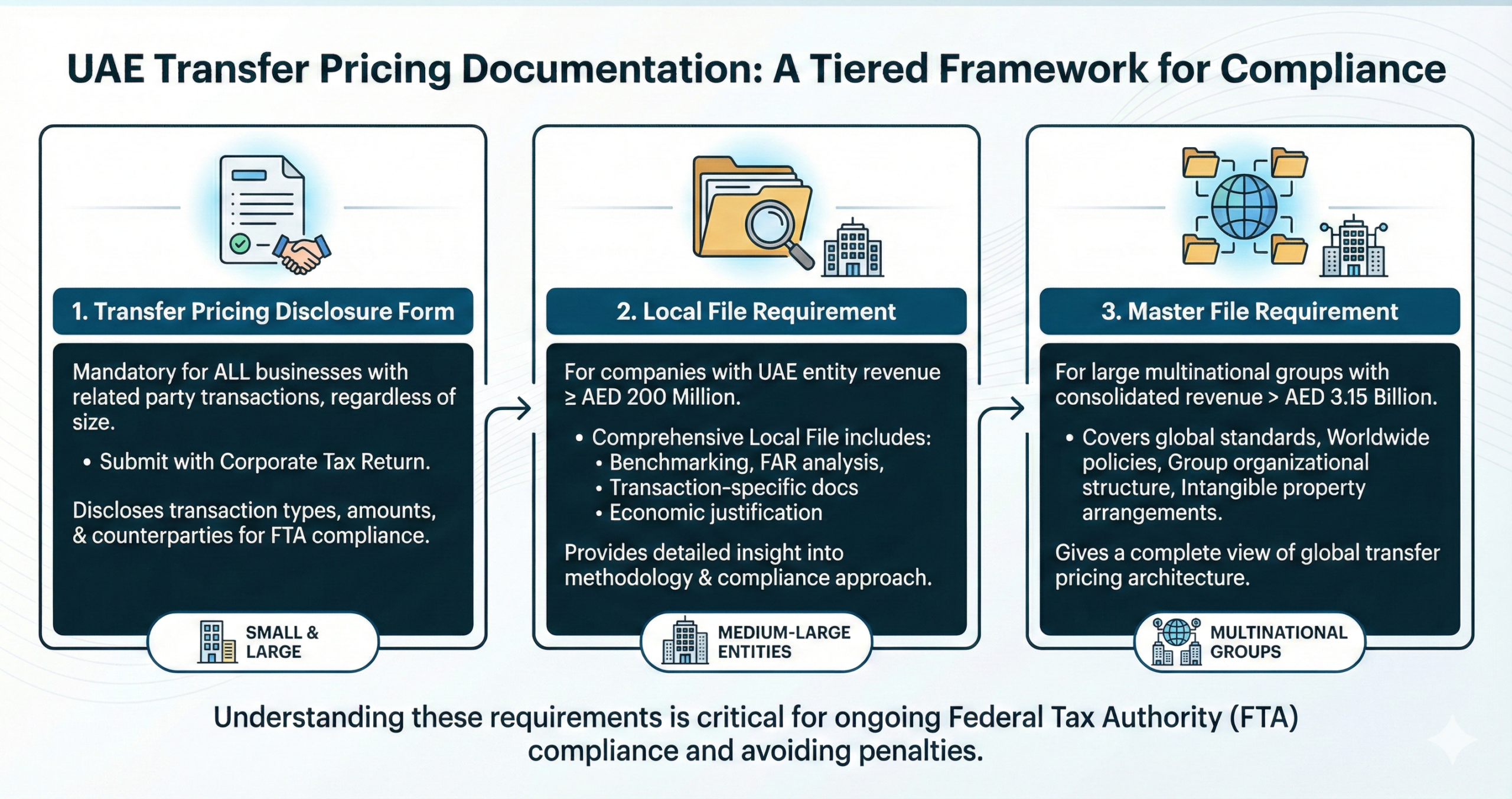

The Federal Tax Authority (FTA) has established a tiered documentation framework that applies to businesses based on their size and transaction volumes. Understanding these requirements is critical for compliance.

Transfer Pricing Disclosure Form

This form is mandatory for ALL businesses with related party transactions, regardless of size. It must be submitted with your Corporate Tax Return and includes disclosure of transaction types, amounts, and counterparties. Even small businesses with minimal related-party dealings must complete this form to maintain FTA compliance.

Local File Requirement

Companies with UAE entity revenue of AED 200 million or more must prepare a comprehensive Local File. This document includes detailed benchmarking analysis, functional analysis and risk assessment (FAR analysis), transaction-specific documentation, and economic justification for pricing policies. The Local File provides the FTA with detailed insight into your transfer pricing methodology and compliance approach.

Master File Requirement

Large multinational groups with consolidated revenue exceeding AED 3.15 billion must prepare a Master File. This document covers global benchmarking standards, worldwide transfer pricing policies, group organizational structure, and intangible property arrangements. The Master File gives regulators a complete view of the group’s global transfer pricing architecture.

Understanding the Compliance Imperative

The Federal Tax Authority (FTA) now requires businesses to demonstrate that their related-party transactions comply with the Arm’s Length Principles global standard aligned with OECD transfer pricing guidelines. This principle mandates that terms and conditions between related entities must mirror those that would exist between independent parties operating under comparable circumstances.

The regulatory shift has created four critical compliance challenges:

- Audit Requirements: External auditors increasingly demand benchmarking evidence before signing off on financial statements. Without proper documentation, companies face audit delays, qualified opinions, or outright refusals.

- Tax Filing Integrity: Unsupported transactions create vulnerabilities in corporate tax returns. The FTA may challenge pricing that appears inconsistent with market rates, triggering adjustments and potential penalties.

- Deduction Protection: Without third-party validation, expenses such as management fees, executive compensation, or inter-company charges may be disallowed, resulting in higher taxable income.

- Integrated Governance: Benchmarking serves multiple functions simultaneously ensuring accounting accuracy, facilitating audit readiness, and maintaining tax compliance across all business operations.

Transfer Pricing Benchmarking Methodology

The UAE follows OECD transfer pricing guidelines, which recognize five primary methods for establishing arm’s length pricing. Understanding these methodologies is essential for proper compliance.

TNMM (Transactional Net Margin Method)

The TNMM is the most widely used method in UAE benchmarking reports, applied in over 80% of cases. This method compares the net profit margin of a tested party against the margins earned by comparable independent companies performing similar functions. TNMM is particularly effective for service companies, distributors, and management fee arrangements where profit margins provide reliable comparison points.

Other OECD Methods

Comparable Uncontrolled Price (CUP) Method: Compares the price charged in a controlled transaction to prices in comparable uncontrolled transactions. Most reliable when identical products or services exist in the market.

Cost Plus Method: Adds an appropriate markup to the costs incurred by the supplier in a controlled transaction. Commonly used for manufacturing or service provision arrangements.

Resale Price Method: Subtracts an appropriate gross margin from the resale price to unrelated parties. Typically used for distribution arrangements.

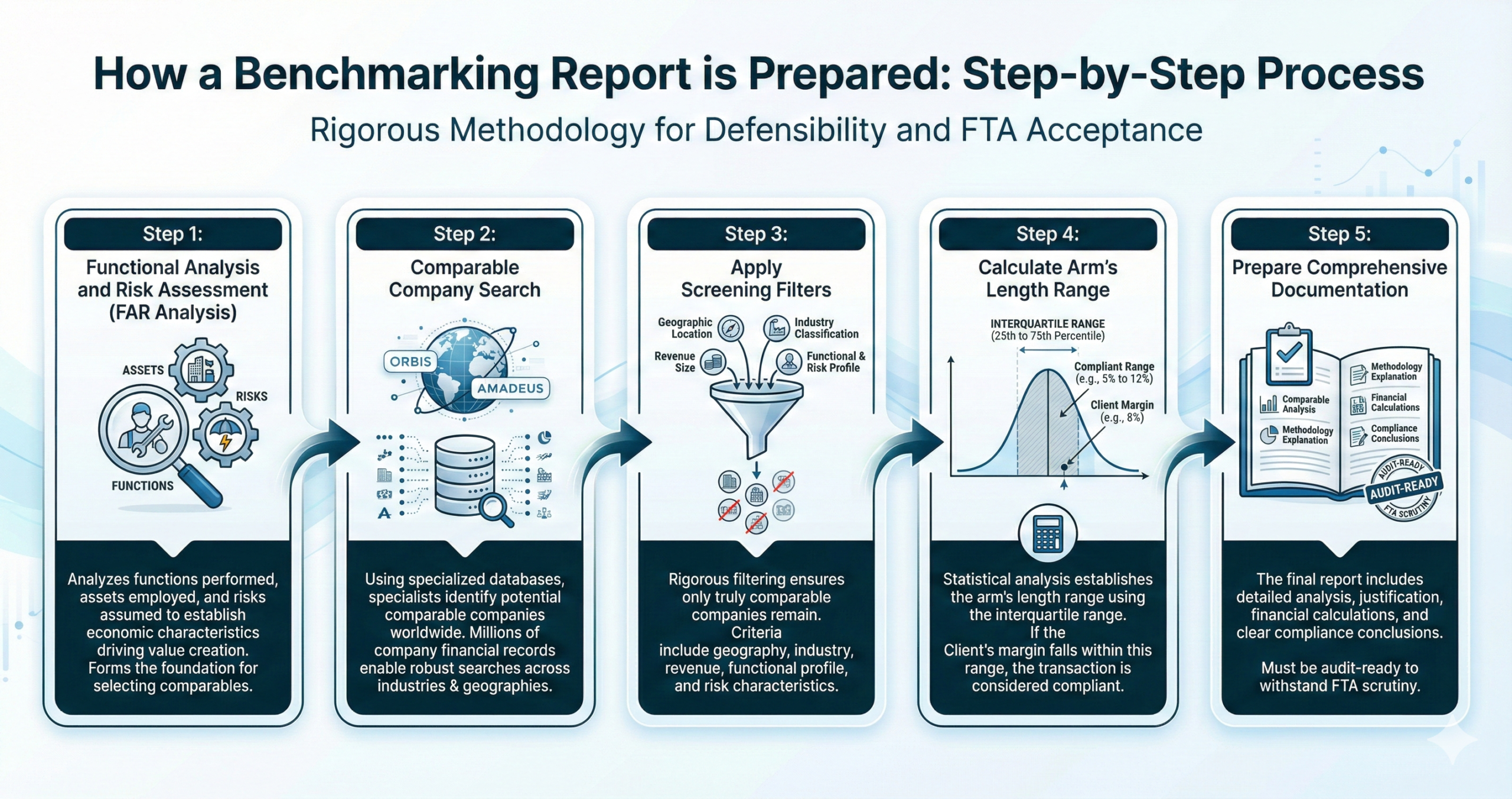

How a Benchmarking Report is Prepared: Step-by-Step Process

Professional benchmarking reports follow a rigorous methodology to ensure defensibility and FTA acceptance. Here’s how the process works:

Step 1: Functional Analysis and Risk Assessment (FAR Analysis)

The first step involves comprehensive analysis of the functions performed, assets employed, and risks assumed by each party to the transaction. This FAR analysis establishes the economic characteristics that drive value creation and forms the foundation for selecting appropriate comparables.

Step 2: Comparable Company Search

Using specialized databases such as Orbis and Amadeus, transfer pricing specialists identify potentially comparable companies. These databases contain financial information on millions of companies worldwide, enabling robust comparable searches across industries and geographies.

Step 3: Apply Screening Filters

Potential comparables undergo rigorous filtering based on geographic location, industry classification, revenue size, functional profile, and risk characteristics. This ensures that only truly comparable companies remain in the final analysis set.

Step 4: Calculate Arm’s Length Range

Statistical analysis of the comparable set establishes the arm’s length range, typically using the interquartile range (25th to 75th percentile). For example, if market margins range from 5% to 12% and the client’s margin is 8%, the transaction falls within the compliant range.

Step 5: Prepare Comprehensive Documentation

The final benchmarking report includes detailed comparable company analysis, methodology explanation and justification, financial calculations and statistical analysis, and clear compliance conclusions. This documentation must be audit-ready and capable of withstanding FTA scrutiny.

Transactions Requiring Benchmarking Documentation

The scope of benchmarking extends well beyond large international transactions. UAE businesses must evaluate and document the following arrangements:

- Compensation structures for directors, executives, and key management personnel

- Cross-border service agreements and technical assistance arrangements

- Intra-group financing, loans, and interest rate determinations

- Management, consulting, or administrative service fees

- Royalty payments and intellectual property licensing agreements

- Cost-sharing arrangements and intra-group trading activities

Each transaction type requires comparison against comparable third-party market data to establish compliance with arm’s length standards.

The Connected Persons Risk Factor

The UAE’s current absence of personal income tax creates unique compliance risks. Payments to connected persons including business owners, family members, or key shareholders present heightened scrutiny from regulators. The FTA recognizes that inflated compensation packages could represent profit shifting strategies designed to minimize corporate tax liability.

Without robust benchmarking analysis demonstrating market rate compensation, the FTA may disallow tax deductions for amounts deemed excessive. This transforms what appears to be a legitimate business expense into a non-deductible distribution, fundamentally altering the company’s tax position.

Consequences of Inadequate Documentation

The risks associated with missing or insufficient benchmarking documentation extend across multiple dimensions:

- Immediate Financial Impact: Disallowed deductions increase taxable income, while adjustments to previously filed returns may trigger reassessments for multiple tax years.

- Penalties and Interest: Tax underpayments resulting from inadequate transfer pricing documentation incur financial penalties and interest charges that compound over time.

- Audit Complications: External auditors may qualify their opinions or delay report issuance, creating cascading problems for stakeholders, lenders, and investors.

- Reputational Damage: Tax disputes and qualified audit reports undermine stakeholder confidence and may impact business relationships, financing terms, or partnership opportunities.

- Operational Disruption: Tax authority investigations consume management time and resources while creating uncertainty about financial planning and business strategy.

Establishing a Compliance Framework

Companies seeking to maintain audit readiness and regulatory compliance should implement the following practices:

- Comprehensive Transaction Mapping: Conduct annual reviews to identify all related-party and connected-person transactions across the organization.

- Documentation Gap Analysis: Assess existing benchmarking reports to determine adequacy and identify areas requiring updated or new analysis.

- Regular Update Cycles: Commission fresh benchmarking reports annually or whenever transaction terms undergo material changes to ensure ongoing compliance.

- Early Expert Engagement: Involve transfer pricing specialists and tax advisors during transaction planning, particularly for complex or cross-border arrangements.

- Quality Documentation Standards: Maintain thorough, defensible benchmarking analyses that align with current OECD guidelines and UAE regulatory expectations.

These practices transform compliance from a reactive burden into a proactive governance advantage, strengthening internal controls while satisfying external requirements.

Summary

Benchmarking reports represent far more than compliance paperwork; they constitute essential business infrastructure in the UAE’s evolving regulatory environment. These analyses protect companies from tax adjustments, facilitate smooth audits, and demonstrate commitment to transparent financial governance. By ensuring that executive compensation, inter-company transactions, and connected-party arrangements conform to global transfer pricing standards, businesses establish credibility with regulators, auditors, and stakeholders alike.

Companies that prioritize proper benchmarking documentation position themselves for sustainable success in the UAE’s new corporate tax landscape, transforming regulatory requirements into competitive advantages through enhanced governance and financial transparency.

How ebs Chartered Accountants Can Support Your Compliance Journey

ebs chartered accountants in dubai can deliver comprehensive benchmarking reports specifically designed for UAE Corporate Tax and transfer pricing regulations, ensuring full compliance with the Arm’s Length Principle. Our team of specialists provides defensible documentation, rigorous comparable market analysis, and audit-ready reports that help companies minimize tax risk and confidently satisfy Federal Tax Authority requirements.

FAQs

What exactly is a benchmarking report and why is it required in the UAE?

A benchmarking report independently compares your related-party transactions against market rates between unrelated entities. Under UAE corporate tax law (Federal Decree-Law No. 47 of 2022), businesses must prove transactions comply with the Arm’s Length Principle to prevent profit shifting.

Which specific transactions require benchmarking documentation?

Benchmarking is required for transactions between related parties including executive compensation, management fees, intra-group loans, cross-border services, royalty payments, and cost-sharing agreements. Even routine arrangements like owner salaries now require market-rate validation.

Q3: How often should benchmarking reports be updated?

Best practice requires annual benchmarking updates to reflect current market conditions. Reports should also be refreshed when transaction terms change materially, as auditors and the FTA expect current, relevant documentation.

What are the consequences if our company doesn’t have proper benchmarking documentation?

Companies risk disallowed tax deductions, higher taxable income, and FTA adjustments with penalties and interest. External auditors may delay or qualify financial statements, damaging reputation and triggering costly tax disputes.

Can we prepare benchmarking reports internally, or do we need external specialists?

While internal preparation is possible, the FTA and auditors expect professional rigor using specialized databases and OECD expertise. External specialists provide objectivity, technical knowledge, and credibility crucial for defending documentation during audits.