From 1 January 2026, the UAE introduced a major reform to excise tax on sweetened drinks. The system has moved away from a flat 50% tax based on price and shifted to a tiered, volumetric-based tax linked directly to sugar content. Under the new rules, excise tax is charged as a fixed amount per litre, with rates ranging from zero to AED 1.09 per litre, depending on how much sugar or sweetener a drink contains. This change significantly affects how beverages are classified, tested, priced, and reported.

Legal Framework

The reform is set out in Cabinet Decision No. 197 of 2025 (issued 27 November 2025) and implemented through FTA Decisions No. 10 and 11 of 2025 (issued 12 December 2025). Further guidance is provided through FTA public clarifications (EXTP012 and EXTP013) and technical testing guidelines issued by the Ministry of Industry and Advanced Technology (MoIAT).

The previous regime under Cabinet Decision No. 52 of 2019 has been repealed. Notably, the separate category for “carbonated drinks” has been removed; carbonation is no longer relevant. Sugar content is now the only basis for classification.

What Qualifies as a Sweetened Drink?

A sweetened drink is any beverage to which sugar, artificial sweeteners, or other sweetening agents have been added and which is intended for consumption as a drink. This includes ready-to-drink products, concentrates, powders, syrups, gels, extracts, and products that can be converted into a drink.

Important: Products that contain only naturally occurring sugar, such as 100% fruit juice with no added sweeteners, are not considered sweetened drinks and are not subject to excise tax.

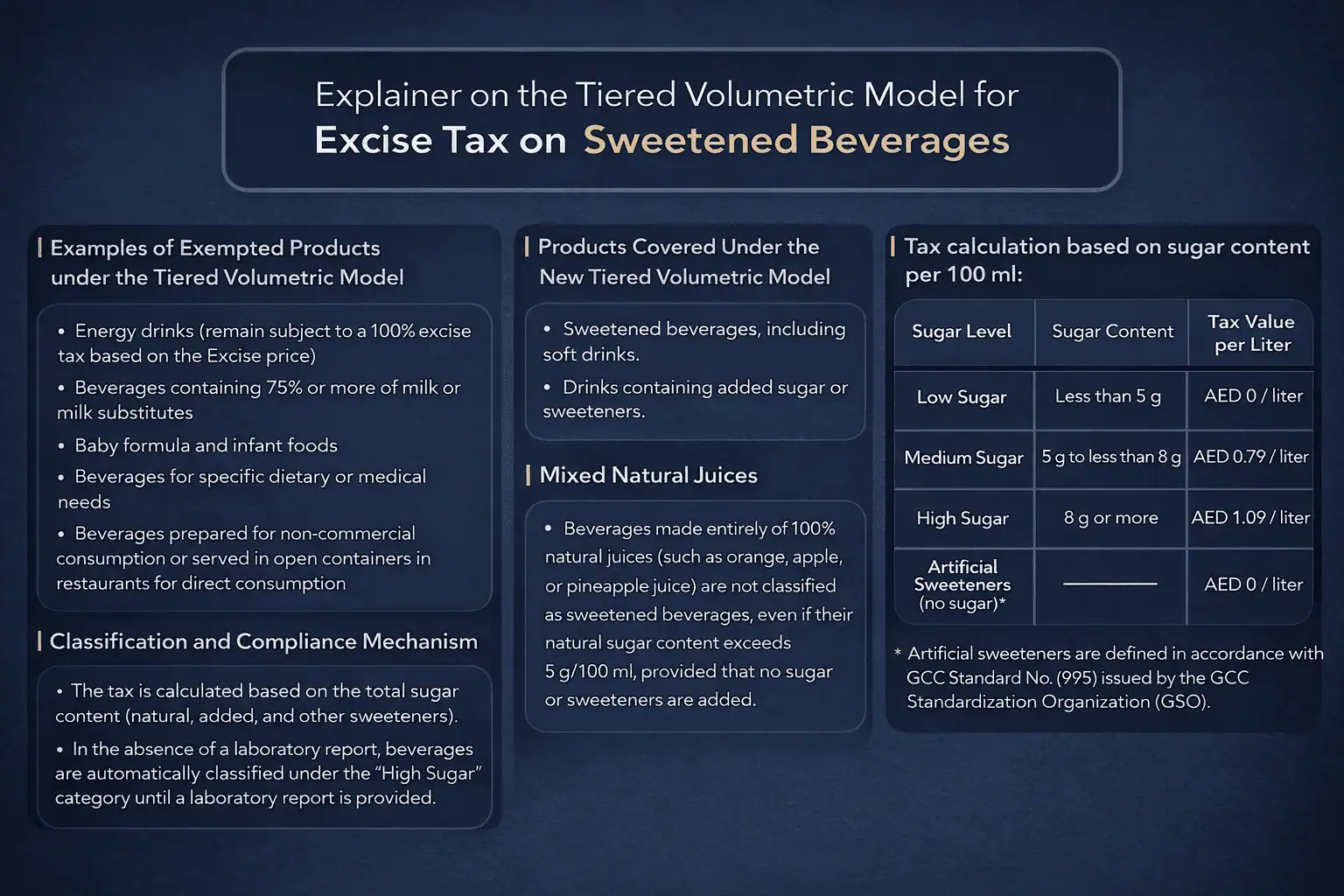

Key Exclusions

The following categories are excluded from the definition of sweetened drinks:

- Milk-based beverages (at least 75% milk in ready-to-drink form)

- Milk substitute beverages (at least 75% milk alternatives, subject to calcium requirements)

- Baby products (infant formula, follow-up formula, baby food)

- Special dietary beverages (as per GCC Standard 654)

- Medical nutrition products (as per GCC Standard 1366)

- Drinks prepared in restaurants for immediate consumption and served in open containers

Tax Categories and Rates

The new excise framework introduces a tiered volumetric model, where excise tax is calculated per litre based solely on sugar content per 100 ml of the finished beverage.

Tiered Volumetric Excise Tax Rates for Sweetened Drinks

| Category | Sugar Content (per 100 ml) | Basis of Classification | Excise Tax Rate | Compliance Status |

| High Sugar | ≥ 8 g | Total sugar (added + naturally occurring) | AED 1.09 per litre | Fully taxable |

| Moderate Sugar | ≥ 5 g to < 8 g | Total sugar (added + naturally occurring) | AED 0.79 per litre | Fully taxable |

| Low Sugar | < 5 g | Total sugar below threshold | AED 0.00 per litre | Zero-rated (full compliance required) |

| Artificially Sweetened | 0 g sugar, contains artificial sweeteners only, or artificial sweeteners with < 5 g sugar | Classification driven by presence of artificial sweeteners | AED 0.00 per litre | Zero-rated (full compliance required) |

Even where the excise tax rate is zero, full compliance obligations still apply, including laboratory testing, MoIAT certification, excise goods registration, and excise tax return filing with the FTA.

SugarCalculation Rules

If a drink contains any added sweetener, all sugar including naturally occurring sugaris counted when determining the tax category.

- 100% juice with no additives: not taxable

- The same juice with added sugar: total sugar applies, potentially placing it in the highest category

Artificial sweeteners are not measured in grams for tiering purposes, but their presence affects classification. Other sweeteners such as honey, agave, or maple syrup are counted as sugar.

Mandatory Laboratory Testing

All sweetened drink products must be tested by an ISO/IEC 17025 accredited laboratory.

- Products claiming to be 100% natural juice must undergo HPLC, IRMS (to prove no added sugar), and artificial sweetener testing.

- Only two UAE labs currently offer IRMS testing: ADQCC and SGS Gulf.

- Other sweetened drinks require HPLC and artificial sweetener testing.

Test results must be shown in grams per 100ml, are valid for one year, and apply across all pack sizes of the same product (but not different flavours).

MoIAT Certificate of Conformity

Before products can be registered on the FTA’s EmaraTax platform, a Certificate of Conformity must be obtained from MoIAT.

- Cost: AED 1,290 per certificate

- Processing time: typically 2–3 working days

- Applications are submitted through the MoIAT ECAS portal

Concentrated Products

For powders or syrups without clear or accurate preparation instructions, the FTA applies a standard calculation formula based on maximum possible dilution. In these cases, tax is generally applied at the moderate rate (AED 0.79 per litre), regardless of actual sugar content, with limited exceptions.

Transitional Relief (1 Jan – 30 Jun 2026)

Businesses that initially paid tax at the highest rate due to missing laboratory certificates may claim deductions if they later obtain valid certification showing a lower tax category or zero rate.

Relief is only available if strict conditions are met, and no claims will be accepted after 30 June 2026.

Compliance Risk

Products registered without valid laboratory certificates are automatically treated as high-sugar drinks until proper documentation is submitted. This is a default compliance mechanism, not a penalty.

Key Dates

- 27 November 2025 – Cabinet Decision issued

- 12 December 2025 – FTA Decisions issued

- 1 January 2026 – New system takes effect

- 30 June 2026 – Transitional relief ends

Conclusion

The new excise tax framework introduces a clearer, more predictable system that directly links tax to sugar content. It encourages reformulation, rewards lower-sugar products, and relies on objective laboratory testing to ensure consistency.

Businesses should act early to complete testing, obtain certifications, and update registrations. While the transitional relief period offers some flexibility, it is time-limited and will not extend beyond June 2026.

How ebs Chartered Accountants Can Help

ebs Chartered Accountants supports businesses at every stage of excise tax compliance. This includes:

- Excise tax advisory and product classification

- Coordination with accredited laboratories for mandatory testing

- Assistance with MoIAT Certificates of Conformity

- Product registration on the FTA’s EmaraTax platform

- Preparation and filing of excise tax returns

They work closely with finance, operations, and supply chain teams to ensure compliance is handled efficiently and accurately.

Ongoing Excise Tax Support

Beyond initial registration, ebs provides ongoing support, including audit assistance, compliance reviews, and guidance on reformulation strategies. The aim is to help businesses remain compliant without disrupting day-to-day operations or commercial decision-making. For More information Contact us at: www.ebs.ae

Frequently Asked Questions (FAQs)

Are zero-sugar drinks exempt from compliance?

No. Zero-sugar and artificially sweetened drinks are zero-rated for excise tax, but they must still undergo mandatory laboratory testing, obtain MoIAT certification, be registered on EmaraTax, and be reported in excise tax returns.

Is 100% fruit juice subject to excise tax?

Pure 100% fruit juice with no added sugar or sweeteners is not subject to excise tax. However, laboratory testing is required to prove that no sugar or artificial sweeteners have been added.

What happens if a product is registered without a lab certificate?

If no valid laboratory certificate is submitted, the product is automatically classified as a high-sugar drink. Excise tax will be applied at the highest rate until proper documentation is provided.

How often must laboratory testing be renewed?

Laboratory testing must be renewed every 12 months. Updated test reports are required to maintain correct tax classification and ongoing compliance with FTA requirements.

Can excise tax overpaid during the transition period be recovered?

Yes. Overpaid excise tax can be claimed as a deduction if valid certificates are later obtained, provided all FTA conditions are met and claims are submitted by 30 June 2026.