More than 70% of UAE small businesses struggle with bookkeeping accuracy in their first two years. Many lose money not because of poor sales but because of disorganised financial records, missed VAT filing deadlines, and payroll errors that pile up quietly in the background.If you run a small business in Dubai or anywhere in the UAE, the right client bookkeeping solution can save you thousands of dirhams annually and protect you from FTA penalties.

This guide breaks down exactly what client bookkeeping solutions are, how to choose the right one for your business, and how to set it up properly in 2026 with UAE corporate tax and VAT compliance built in from day one.

What Are Client Bookkeeping Solutions?

Client bookkeeping solutions are systems, services, or software setups that manage a business’s day-to-day financial records including income, expenses, payroll, VAT filings, and financial reporting.

They come in three forms:

- Software-only: You manage your own books using tools like Zoho Books, QuickBooks, or Xero.

- Outsourced: A professional accounting firm handles everything for you.

- Hybrid: You use software, with part-time expert support for complex tasks like tax filing.

For UAE small businesses, the stakes are high. The Federal Tax Authority (FTA) requires VAT-registered businesses to maintain accurate records for a minimum of five years under Federal Decree-Law No. 47 of 2022. A weak bookkeeping setup puts your entire compliance position at risk.

Why Bookkeeping Matters More in 2026

2026 brings new urgency to bookkeeping for UAE businesses. Corporate tax compliance requirements have expanded. Free zone businesses face tighter Economic Substance Regulation (ESR) audits. And AI-powered fraud detection by the FTA means manual errors are spotted faster than ever.

Three shifts define the 2026 bookkeeping landscape:

- Corporate tax filing: Businesses must now file annual corporate tax returns. Your books need to match your tax position exactly.

- AI-assisted audits: The FTA uses automated reconciliation tools. Mismatches between VAT returns and your books trigger reviews.

- E-invoicing mandates: Digital invoice submission is expanding across UAE jurisdictions. Your accounting system must support this.

How to Choose the Right Client Bookkeeping Solution for Your Business

The right choice depends on your business size, transaction volume, and in-house accounting capacity. Here is a breakdown:

| Solution Type | Best For | Key Benefit | 2026 Watch-Out |

|---|---|---|---|

| Software Only (Zoho, QBO) | Solo founders, freelancers | Low cost, auto VAT filing | No expert advice for CT filings |

| Outsourced Accounting | SMEs with 5–50 staff | Full compliance, saves AED 10K+/year vs in-house | Choose an FTA-registered firm |

| Hybrid Model | Growing e-commerce, free zone cos. | Scalable, flexible expert access | Ensure software integrates with auditor |

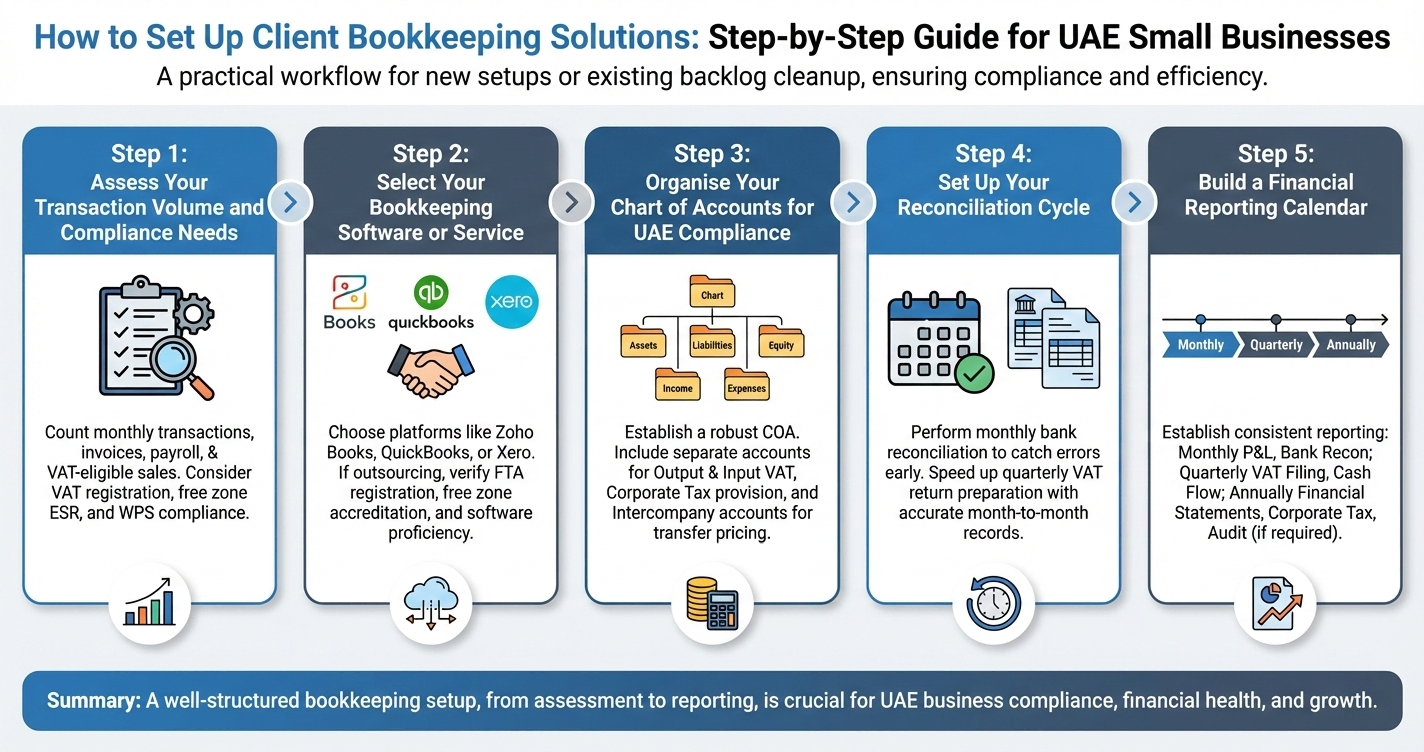

How to Set Up Client Bookkeeping Solutions: Step-by-Step

Below is a practical setup workflow for UAE small businesses whether you are starting from scratch or cleaning up an existing backlog.

Step 1: Assess Your Transaction Volume and Compliance Needs

Start by counting your monthly transactions, invoices issued, vendor payments, payroll runs, and VAT-eligible sales. A business with under 100 transactions per month can often run a lean software-only setup. Anything above that typically benefits from outsourced or hybrid support.

Ask yourself:

- Are you VAT-registered? If yes, your records must support quarterly VAT return filing.

- Do you operate in a free zone? ESR compliance adds reporting requirements.

- Do you have employees? WPS (Wage Protection System) payroll compliance is mandatory.

Step 2: Select Your Bookkeeping Software or Service

For UAE businesses, Zoho Books is the most widely used platform; it supports multi-currency transactions, automatic VAT calculations, and direct integration with UAE bank feeds. QuickBooks and Xero are solid alternatives, particularly for businesses with international clients.

If you go the outsourced route, confirm that your accounting firm is:

- Registered with the FTA as an approved tax agent.

- Accredited to audit in your free zone (DMCC, JAFZA, DIFC, RAKEZ, etc.).

- Proficient in the accounting software you use, so data hand-offs are seamless.

Step 3: Organise Your Chart of Accounts for UAE Compliance

A chart of accounts (COA) is the backbone of your bookkeeping system. It categorises every financial transaction into asset, liability, equity, income, and expense buckets.

For UAE compliance, your COA must include:

- Separate accounts for output VAT (5%) and input VAT to support clean VAT return preparation.

- A corporate tax provision account, now that the 9% CT rate applies to taxable income above AED 375,000.

- Intercompany accounts if your business has related-party transactions these require transfer pricing documentation.

Step 4: Set Up Your Reconciliation Cycle

Reconciliation means matching your accounting records against your bank statements. Do this monthly not quarterly. Monthly reconciliation catches data entry errors, duplicate payments, and missing invoices before they compound into audit problems.

A clean monthly reconciliation cycle also speeds up your VAT return preparation dramatically. When your records are accurate month-to-month, the quarterly filing becomes a 30-minute task instead of a week-long scramble.

Step 5: Build a Financial Reporting Calendar

Consistent reporting keeps your business financially healthy. Here is a baseline reporting calendar for UAE small businesses:

- Monthly: Profit & loss statement, bank reconciliation, accounts receivable aging.

- Quarterly: VAT return filing (FTA deadline: 28 days after quarter-end), cash flow review.

- Annually: Financial statements, corporate tax return, external audit (if required by your free zone).

Real Example: How StableGrowz Got Its Books in Order

StableGrowz, a Dubai-based business consulting firm, was managing its own accounting manually and struggling to keep up with VAT filings and tax deadlines. The workload was manageable at first but as the company grew, the gaps in its bookkeeping became costly.

They brought in ebs Chartered Accountants for ongoing accounting and tax filing services. The decision came down to one factor: ebs had a verified track record on independent review platforms, which gave StableGrowz confidence before signing.

The engagement involved a 2-to-5 person team from ebs, handling everything from monthly bookkeeping to quarterly VAT returns. The CEO of StableGrowz was so satisfied with the outcome that he recommended ebs to other businesses in his network.

The takeaway is simple: when bookkeeping is handled by a dedicated, qualified team, business owners stop firefighting financial errors and start making decisions based on accurate data.

Common Bookkeeping Mistakes UAE Small Businesses Make

Knowing what not to do is just as valuable as knowing what to do. Here are the four most common bookkeeping errors ebs sees in UAE small businesses:

- Mixing personal and business expenses. This is the number one issue in sole proprietorships. It makes VAT reconciliation nearly impossible and raises red flags during audits.

- Delaying VAT registration. If your taxable supplies exceed AED 375,000 in any 12-month period, VAT registration is mandatory. Late registration carries FTA penalties.

- Using free tools without UAE VAT support. Tools like Wave Accounting do not natively support UAE VAT structures. Switching later creates data migration headaches.

- Ignoring backlog accounting. Many businesses skip months of bookkeeping during busy periods, then face a backlog that is expensive to clean up before audit season.

When Should You Outsource Your Bookkeeping?

Outsourcing your bookkeeping makes financial sense when the cost of errors exceeds the cost of the service. In most UAE SME scenarios, outsourcing to a qualified firm saves between AED 8,000 and AED 15,000 per year compared to hiring a part-time in-house bookkeeper once you factor in employment visa costs, benefits, and ongoing training.

Signs that it is time to outsource:

- Your VAT filings are consistently late or require corrections.

- You do not have a clear picture of your monthly cash flow.

- You are scaling and your transaction volume has outgrown a spreadsheet.

- Your free zone has requested audited financial statements.

ebs Chartered Accountants offers outsourced accounting and bookkeeping packages built specifically for UAE SMEs with full Zoho Books setup, VAT compliance, payroll processing, and dedicated accountant access. Their team has supported 500+ businesses across Dubai and the wider UAE since 2017.

Contact ebs for a Free 2026 Bookkeeping Audit

Your bookkeeping setup directly affects your tax position, audit readiness, and business decisions. If you are not confident that your current system is built for UAE compliance in 2026, it is worth finding out before the FTA does.

ebs Chartered Accountants has helped 500+ businesses across Dubai and the UAE build clean, compliant, and scalable bookkeeping systems. The team holds Big 4 experience, holds an advanced Zoho partner accreditation, and is an approved auditor in every major UAE free zone.

Book your free 2026 bookkeeping audit today: Schedule a call with ebs →

Frequently Asked Questions

What are client bookkeeping solutions for small businesses?

Client bookkeeping solutions are systems that track a business’s financial transactions including income, expenses, VAT, and payroll. They can be software tools, outsourced accounting services, or a combination of both. For UAE small businesses, the right setup ensures FTA compliance and accurate financial reporting.

Is outsourced bookkeeping worth it for a small UAE business?

Yes for most UAE SMEs, outsourced bookkeeping costs less than in-house hiring once visa and employment costs are included. It also brings specialist knowledge of UAE VAT, corporate tax, and free zone compliance that a general bookkeeper may not have.

What bookkeeping software works best for UAE VAT compliance?

Zoho Books is the most widely recommended platform for UAE businesses. It supports 5% VAT auto-calculation, AED multi-currency transactions, and integrates with UAE bank feeds. QuickBooks and Xero are strong alternatives, especially for businesses with international operations.

How often should a UAE small business reconcile its accounts?

Monthly reconciliation is the standard best practice. It catches errors early, keeps your VAT records clean for quarterly filings, and reduces the workload during annual audit season. Waiting until year-end significantly increases the risk of costly corrections.

Do UAE free zone businesses need an external audit?

Most UAE free zones including DMCC, JAFZA, DIFC, and RAKEZ require annual audited financial statements from an approved auditor. Mainland companies also need audited accounts for certain regulatory submissions. ebs is an approved auditor across all major UAE free zones.

What happens if I miss a VAT filing deadline in the UAE?

Late VAT filing triggers FTA administrative penalties starting at AED 1,000 for the first offence, rising to AED 2,000 for repeat cases. Interest charges also apply on unpaid VAT. A structured client bookkeeping solution with calendar reminders prevents these penalties entirely.