On 29 September 2025, the UAE Ministry of Finance (MoF) issued Ministerial Decision No. 243 of 2025 and Ministerial Decision No. 244 of 2025, marking a major milestone in the country’s digital transformation. These decisions define the scope, obligations, and phased implementation of the new UAE Electronic Invoicing (E-Invoicing) System. Both Ministerial Decisions will become effective upon their publication in the Official Gazette. This blog explains the key details from both ministerial decisions, including scope, exclusions, deadlines, and implementation rules, plus how businesses can prepare for compliance.

E-Invoicing Decisions

Ministerial Decision No. 243 of 2025 defines the scope of the Electronic Invoicing System (EIS), together with which transactions are covered and which might be expressly excluded for now. Ministerial Decision No. 244 of 2025 lays out the targeted regulations for implementation. Together, they set up an obligatory E-Invoicing framework for B2B and B2G transactions, introducing new compliance requirements that UAE businesses must follow.

What Is E-Invoicing?

E-invoicing refers to a standardized digital format of invoice data that is exchanged electronically between the issuer and the recipient. Under the UAE EIS, these data need to additionally be sent to the Federal Tax Authority (FTA) in real-time or close to real-time, ensuring accuracy, transparency, and more suitable tax compliance across transactions.

Scope of the UAE E-Invoicing System

The system applies to all Persons conducting Business in the UAE for every Business Transaction, unless specifically excluded.

Included

- B2B (Business-to-Business) transactions

- B2G (Business-to-Government) transactions

Excluded for Now

- B2C (Business-to-Consumer) transactions

Businesses dealing exclusively with consumers are not yet required to issue e-invoices. A future ministerial decision will introduce B2C requirements.

Excluded Transactions

The following transactions are exempt from mandatory e-invoicing:

Government Entities

Transactions carried out by government bodies in their sovereign or regulatory capacity, where they are not competing with the private sector, are excluded from e-invoicing requirements.

Financial Services

Financial services that are VAT-exempt or zero-rated fall outside the e-invoicing scope under current UAE VAT rules

B2C (Business-to-Consumer) Transactions

Sales made directly to consumers are currently excluded. B2C e-invoicing will only be introduced through future ministerial decisions.

Aviation-Related Transactions

- International passenger travel with an electronic ticket

- Ancillary airline services supported by an Electronic Miscellaneous Document (EMD)

- International air cargo with an Airway Bill (excluded for 24 months from rollout)

Voluntary Participation in the E-invoicing system is permitted even for entities currently excluded enabling early adoption and system familiarization

Phased Rollout and UAE E-Invoicing Timeline

The UAE will roll out the e-invoicing system in three phases, aligned with business size and category:

| Phase | Category | ASP Appointment Deadline | Go-Live Date |

| Pilot Programme

|

Selected taxpayers invited by MoF/FTA (with written consent) | Not required

|

1 July 2026

|

| Voluntary Adoption

|

Any Business | Flexible | From 1 July 2026 |

| Phase 1 | Persons with revenue ≥ AED 50M | 31 July 2026 | 1 January 2027 |

| Phase 2 | Persons with revenue < AED 50M | 31 March 2027 | 1 July 2027 |

| Phase 3 | Government Entities | 31 March 2027 | 1 October 2027 |

Important Note: E-invoicing applies to all entity types, VAT-registered or not. Further, each VAT group member must register separately.

E-Invoice Format Requirements (Mandatory Fields)

Every e-invoice issued in the UAE must comply with FTA specifications and include certain mandatory data elements.

| Field | Requirement |

| Invoice Number | Unique identifier for each invoice. |

| Date of Issue | Date when the invoice is generated. |

| Supplier Details | Name, address, and Tax Registration Number (TRN). |

| Customer Details | Name, address, and TRN (if applicable). |

| Description of Goods/Services | Clear itemization with quantities and unit prices. |

| VAT Amount | Calculated at the applicable rate (e.g., 5%). |

| Total Amount Payable | Sum of goods/services cost plus VAT. |

Note: The Federal Tax Authority has released a detailed E-Invoicing Data Dictionary, which defines the mandatory data fields, technical specifications, and standards to be followed while exchanging invoices via PEPPOL and reporting to the FTA.

Key Requirements Under the UAE E-Invoicing System

Businesses must comply with the following obligations:

1. Structured Digital Format Only

All invoices and credit notes must be issued, transmitted, received, and processed in a digital structured format compatible with FTA systems.

2. Appointment of an Accredited Service Provider (ASP)

Every business must use an ASP approved by the FTA. The official list will be published by the Ministry.

3. 14-Day Issuance Deadline

E-invoices and credit notes must be issued and transmitted within 14 days of the underlying business transaction. Credit notes must be issued when required in case of price changes, cancellations, and returns.

4. Mandatory Reporting to the FTA

Both the issuer and the recipient must process the invoice within the system and report it according to MoF timelines.

5. Self-Billing and Agent Billing Allowed

Permitted if all relevant VAT conditions are completely met and the specified compliance controls are in place.

6. Record Storage Requirements

All digital records must be stored inside the UAE per the Tax Procedures Law.

7. System Failure Reporting

Any system failure must be reported to the FTA within two business days.

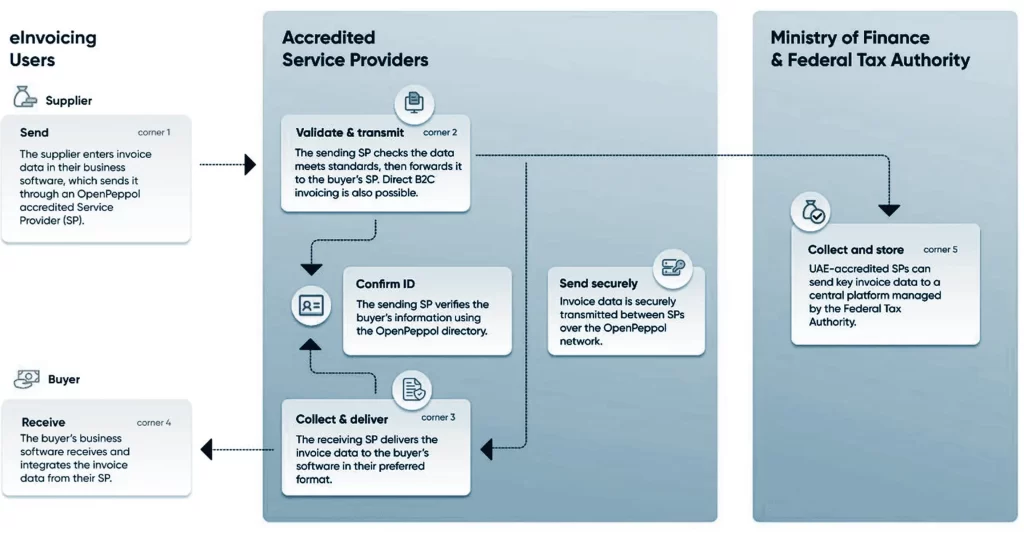

How the UAE E-Invoicing System Works (Peppol 5-Corner Model)

- Seller issues invoice through ERP

- Invoice is transmitted to Seller’s ASP

- ASP validates & converts invoice to PINT AE format

- Invoice sent to Buyer’s ASP

- FTA receives tax data from both sides

- Buyer receives validated invoice and acknowledgment

This model ensures authenticity, data integrity, and secure communication.

Implementation Roadmap

| Step | Title | Key Activities |

| 1 | Assess Tax Positions & Awareness | Review VAT positions, conduct awareness sessions, increase stakeholder visibility |

| 2 | Readiness & Governance | Map IT landscape, assess AR/AP tax logic, identify gaps, define use cases, prepare implementation plan |

| 3 | ASP Selection | Draft RFP, evaluate ASPs, support PoC, shortlist vendors |

| 4 | E-Invoicing Implementation | Sandbox setup, data field mapping, ERP-ASP integration, XML validation |

| 5 | Testing & Go-Live | UAT, team training, correction cycles, deployment, monitoring |

Benefits of E-Invoicing in the UAE

- Reduced errors and improved accuracy

- Better compliance with FTA requirements

- Cost reduction and operational efficiency

- Faster invoice processing and improved cash flow

- Enhanced security and fraud prevention

- Seamless ERP and system integration

- Environmentally sustainable (paperless operations)

How ebs Can Help with UAE E-Invoicing?

ebs chartered accountants in dubai allows businesses seamlessly undertake the UAE e-invoicing system by automating invoice creation, validation, and transmission through FTA-compliant workflows. It ensures complete compliance with MoF requirements, lowering the risk of mistakes. They additionally secure all the digital invoices and credit score notes, simplifying audits and retrieval. Overall, ebs streamlines economic operations, saving significant time and effort.

Conclusion

The UAE’s E-Invoicing System marks a critical move closer to absolutely digitized, transparent, and efficient tax compliance. With obligatory implementation starting 1 January 2027, businesses should:

- Begin preparing internal systems

- Appoint an Accredited Service Provider

- Train teams for smooth adoption

- Participate in the pilot, if applicable

For professional support or system implementation, you can contact us.

FAQs

What is E-Invoicing in the UAE?

E-Invoicing is a digital system requiring businesses to issue and exchange standardized electronic invoices for B2B and B2G transactions, with real-time data reporting to the Federal Tax Authority to enhance tax compliance and transparency.

When does E-Invoicing become mandatory in the UAE?

Mandatory e-invoicing starts on January 1, 2027, initially applying to businesses with annual revenue of AED 50 million or more, followed by phased rollout to smaller businesses and government entities until October 2027.

Which transactions are excluded from UAE E-Invoicing requirements?

The system excludes B2C transactions, government entities in sovereign roles, certain financial services, and some aviation-related transactions, with B2C invoicing to be introduced by future ministerial decision.

What are the key requirements for E-Invoicing in the UAE?

Businesses must issue invoices in a structured digital format, appoint an accredited service provider (ASP), issue invoices within 14 days of transaction, and report all e-invoices to the FTA digitally.

What is the timeline and phased rollout for UAE e-invoicing?

The rollout begins with voluntary adoption and a pilot in July 2026, moves to mandatory implementation for large businesses in January 2027, expands to smaller businesses by July 2027, and includes government entities by October 2027.